Under the Building Work Contractors Act 1995 and Regulations, builders performing building work that requires development approval, and has a value of $20,000* or greater, are required to take out a Building Indemnity Insurance (BII) policy on behalf of the homeowner for each and every contract they enter into. Under the Act, the penalties for not taking out appropriate insurance are a $20,000 expiation fee or a penalty of up to $500,000.

* Prior to 10 November 2025, the value of works where BII was required was $12,000 .

If insuring through QBE, builders are required to take out BII on behalf of homeowners through a registered insurance broker. It is strongly advised that builders engage brokers with experience in Building Indemnity Insurance, given the specialised nature of the product.

For information on Assetinsure please click here to access their website.

The following types of work do not require BII.

- Subcontracts to builders contracted to perform the work (the head contractor

must meet any BII requirements) - Contracts solely for demolition work

- Contracts for the SA Housing Authority

- Residential buildings that are over three storeys and contain two or more

separate dwellings - Properties solely used for short-term holiday accommodation

Automatic Eligibility Limit Increases

As part of the Government of South Australia’s BII Reform Package, the Government committed to implementing a process to automatically review and increase builder eligibility limits at regular intervals, to respond to increases in construction costs (Reform 24).

As construction costs increase, builders may find their eligibility limits are reached sooner, putting pressure on their capacity to take on new projects. To help address this, all eligible builders that are insured with QBE will receive a 9% increase to their current eligibility and job profile limits on 1 July 2026, ensuring they can continue to operate effectively and maintain project delivery levels despite cost pressures.

Thereafter, construction costs will be reviewed annually with the intention of applying an increase to builder eligibility and job profile limits on 1 July each year. A range of factors will be considered when determining any increase in future years, and changes to builder eligibility will not necessarily be implemented in every year. Brokers can expect to receive annual correspondence where an increase is to be applied.

For further information builders should contact their registered insurance broker.

Insurance Certificate Data Report

To facilitate the process of seeking alternative insurance, builders and their authorised insurance brokers can obtain a report of their QBE BII certificate data. Certificate information is available for QBE issued policies and projects where the certificate was created on or after 1 January 2018.

To obtain this report please complete this form. Note that you will be asked to provide a current QBE certificate of eligibility to receive the report.

Role of Brokers

Brokers have a vital role in the BII process providing the conduit between builders and the insurer. All certificates taken out through QBE require a registered insurance broker who is approved by QBE to undertake BII operations. Brokers are involved not just for the registration of certificates, but in activities related to builders’ eligibility limits and underwriting reviews.

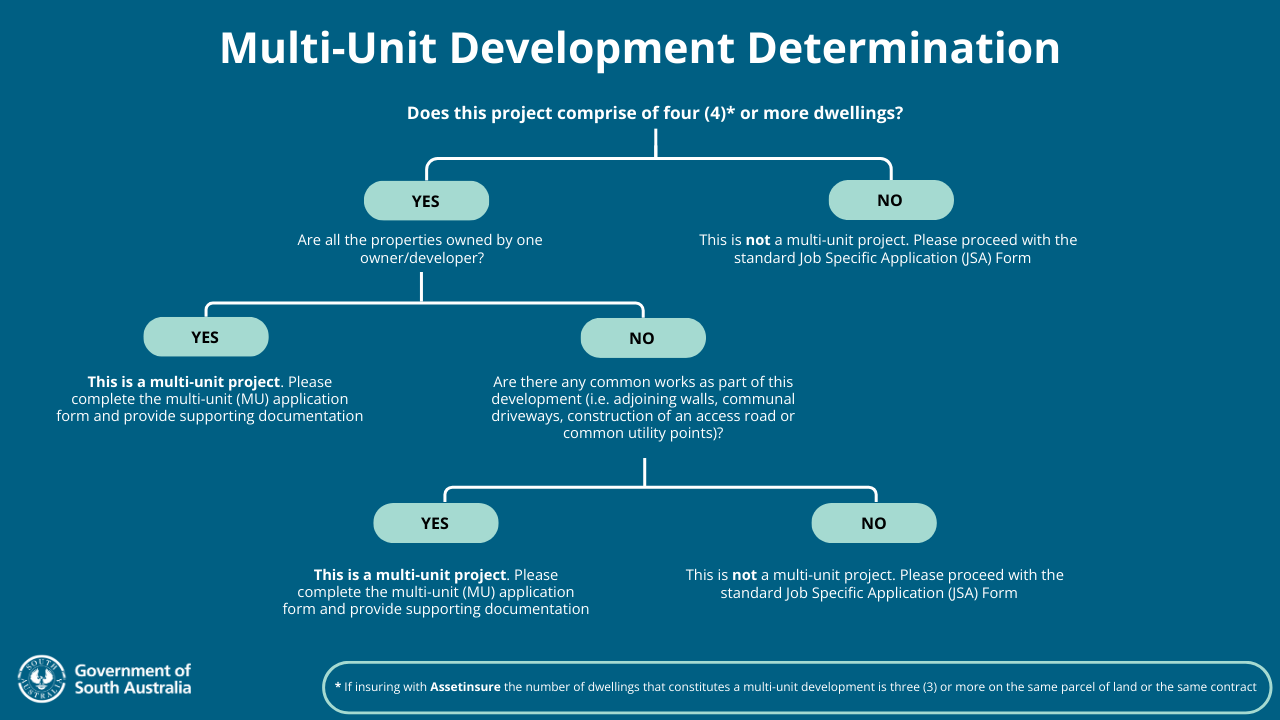

Multi-Unit Developments

The definition of a multi-unit project varies depending on the insurer you are working with. Multi-unit projects follow a different application process and attract different premiums compared to single-dwelling projects.

The flowchart below outlines how to determine whether your building project is classified as multi-unit for BII purposes. Contact your insurer for more information about multi-unit developments.

Builder's Requirements

BII is required to be taken out on any building project of $20,000* or more in value that requires development approval (council approval). If you are unsure whether a project requires BII, please use our BII Helper.

* Prior to 10 November 2025, the value of works where BII was required was $12,000 .

BII cover must be taken out prior to any work beginning on the project. This includes site preparation, demolition, trenching etc.

If a building contract has been entered into before applying for development approval, the builder must take out BII before applying for approval.

To obtain BII, a builder must have a facility with an eligible insurer. To obtain a facility with QBE or Assetinsure, a builder must be licenced to perform building works, then engage an insurance broker, who will work with the insurer to establish the facility.

Click here for insurer contact details.

Yes. The builder taking over is required to take out BII cover, in the same way they would had they been the original builder, to cover the work that the new builder performs.

Builder insurance facilities and limits are managed by the insurer. Any requests or changes should be directed to the appropriate insurer.

If insuring through QBE, builders are required to take out BII on behalf of homeowners through a registered insurance broker. It is strongly advised that builders engage brokers with experience in Building Indemnity Insurance, given the specialised nature of the product. Your insurance broker is the best source to find out what steps need to be taken for eligibility changes.

MBA Rise Program

Master Builders Association South Australia (MBASA) facilitate a program which provides free mentoring and coaching support for South Australia’s Building and Construction Industry. One specific support area relates to growing your business, where experienced industry representatives can provide guidance and tips on BII facility requirements, and the steps required to take to be granted an increased turnover limit with insurers. Click here for more information.